Q3 2024 Dubai Residential Real Estate Market Report

At the start of 2024, I identified two key trends that would shape the year for Dubai’s real estate market: the dominance of the off-plan segment and a recalibration in the market following years of unprecedented growth since Covid. Thus far this year, these projections have started to unfold, and we are seeing it more prominent as reflected in the Q3 data. With 18 years of experience in Dubai’s real estate sector, I apply a meticulous, data-driven approach to cut through market complexities and provide clarity on these topics.

Q3 2024: Beginning of a Turning Point for Dubai’s Real Estate Market

As Dubai’s real estate market continues its growth trajectory, Q3 signified a period of steady evolution and, what I believe, marked the beginning of a pivotal turning point that could shape the market over the next 18-24 months.

The market is adjusting to an influx of new project launches and the gradual introduction of completed supply, a trend that is expected to accelerate in the coming quarters and years. Meanwhile, the secondary market is facing challenges, largely driven by the growing demand and popularity of off-plan sales, which continue to dominate the market and reshape its dynamics. This shift has been further amplified by the transition from a seller’s market to a buyer’s market this year, as buyers become more selective, and sellers remain reluctant to adjust their pricing to meet market expectations. Together, these factors are creating a more competitive environment for the secondary market, with longer transaction cycles and increased pressure to align prices with current demand.

Comprehensive Market Analysis: Beyond Sales Transaction Data

As I mentioned in my Q2 report, it is important to note when evaluating the real estate market, it’s crucial to recognize that sales transaction data, while foundational, doesn’t fully reflect immediate market shifts due to a lag in real-time conditions.

After a deal is agreed upon, it undergoes a detailed transaction process that typically takes 3-4 months to complete. This applies to both secondary market transactions and off-plan registrations. Additionally, the subsequent analysis and reporting of this data add further delays.

To gain a timely and comprehensive understanding of market dynamics, it is essential to consider other data sets such as listing trends, supply levels, demand metrics, mortgage activity, and off-plan developer data. Analyzing these factors in parallel provides a clearer, more accurate picture of the current market landscape.

Let’s dive into the performance of Dubai’s real estate market in Q3 2024, drawing insights from Dubai Land Department open data and analytics provided by REIDIN, a leading real estate data platform in the UAE.

Dubai 2024 Residential Real Estate Overall Summary

Examining year-to-date trends, the secondary market has undergone a significant shift, transitioning from a seller’s market to a buyer’s market. From Q1 to Q2, sales transaction volumes saw a slight decline of 1%, reflecting the initial stages of this adjustment as buyers became more cautious and selective. This was followed by a modest rebound from Q2 to Q3 by 10%, driven by increasing buyer interest as market conditions and secondary supply began to favor purchasers.

However, when looking at the listing data, sellers have been reluctant to align their pricing with market expectations, creating a gap between asking prices and what buyers are willing to pay. This resistance to adjust pricing has contributed to longer days on market, 60 – 90 days depending by area, further emphasizing the shifting balance of power in the secondary market.

The off-plan segment has shown remarkable resilience, with sales transaction volumes increasing significantly, rising by 29% from Q1 to Q2 and by an additional 18% from Q2 to Q3. This sustained growth reflects the strong demand for new developments, fueled by competitive payment plans, developer-driven incentives, and the appeal of modern, future-ready properties. These trends highlight the shifting dynamics within Dubai’s real estate market, where off-plan properties continue to outpace the secondary market, redefining buyer preferences and investment strategies.

Dubai Q3 Residential Real Estate Overall Summary

In Q3 2024, there was an overall total of 48,535 residential sales transactions in Dubai worth AED 119.7B which is an 18% growth from last quarter in volume and 1.4% growth in value.

The shift towards off-plan sales transactions remains prominent in Q3. Of the total transactions, 14,268 occurred in the secondary/ready market, while a significant 34,266 were recorded in the off-plan residential segment.

In the secondary market, there were 11,725 transactions for apartments and 2,544 for villas. Meanwhile, in the off-plan market, apartments dominated with 27,363 transactions, while villas accounted for 6,903 transactions. Across Dubai, the overall price per square foot increased by 3.79% quarter-on-quarter for apartments and by 2.96% for villas.

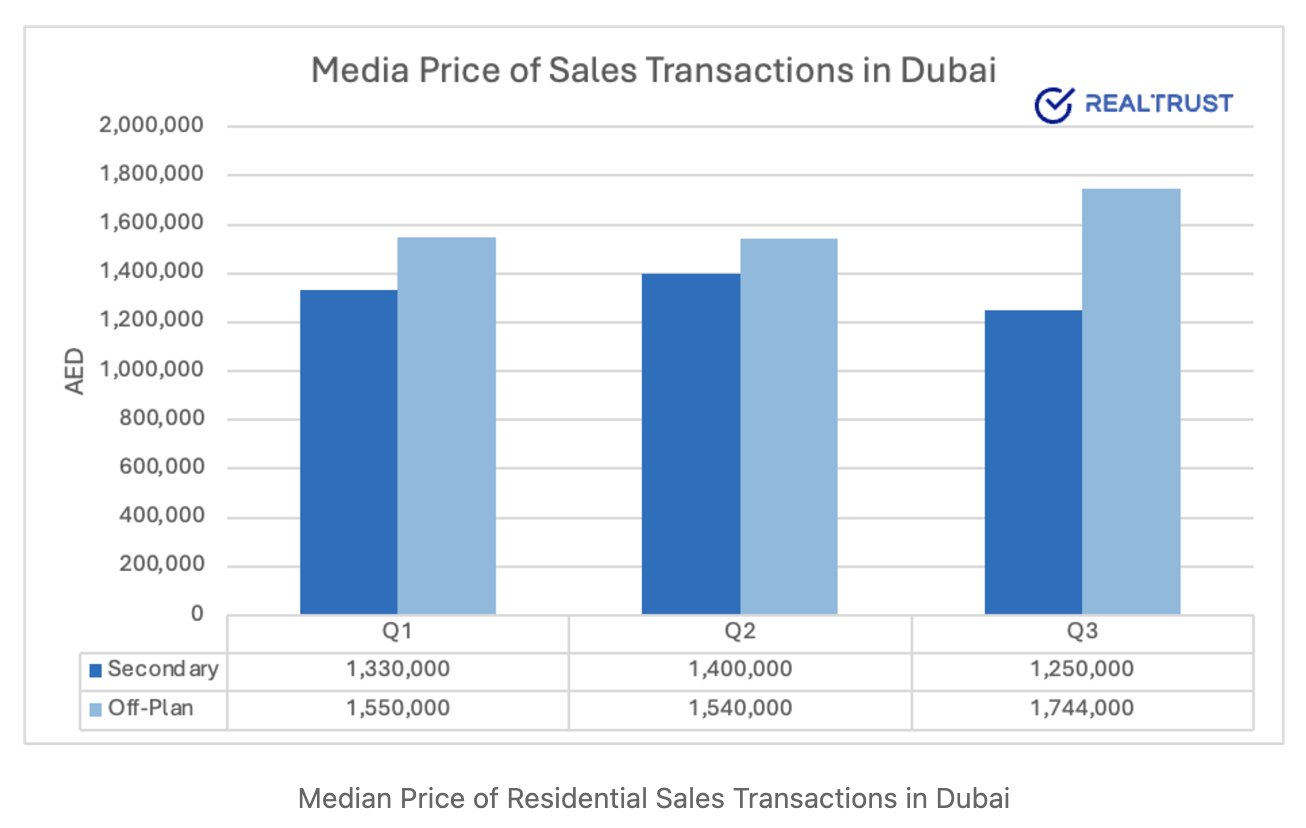

Analyzing the median sale price changes by segment, the secondary market experienced a notable decline of 10.7% in Q3 compared to Q2, while the off-plan market demonstrated robust growth with a 13% increase quarter-on-quarter. This divergence highlights a significant shift in buyer preferences, as the off-plan segment continues to attract strong demand driven by competitive developer incentives and new project launches. Meanwhile, the decline in the secondary market points toward a recalibration in pricing, with listing prices remaining high in certain areas, creating a gap between seller expectations and buyer willingness. In Q3, less than 6% of listings adjusted their prices downward, while days on market continued to stay high, ranging between 60 to 90 days, depending on the area.

It is also noteworthy that 69% of secondary residential transactions in Q3 were mortgaged, compared to 50% in Q2, reflecting a significant increase in mortgage-backed purchases. This trend indicates that more residents are buying properties in the secondary market as their primary residences, rather than for speculative or investment purposes. Such behavior instills confidence in the market, as it demonstrates a growing commitment by residents to make Dubai their long-term home, further solidifying the city’s position as a desirable place to live and invest.

However, it is also worth noting that the decision by some UAE banks to increase mortgage interest rates, despite the U.S. Federal Reserve reducing rates by 25 basis points in early November, is a divergence that may stem from localized financial and economic conditions. This is particularly intriguing given the AED's peg to the U.S. dollar, which typically ensures alignment between U.S. and UAE monetary policies.

Mortgage rates rising in Dubai, despite a global trend of easing, can be attributed to a combination of factors. Banks may be adjusting rates to manage increased demand for mortgages driven by a growing population and strong secondary market mortgage activity, as well as to address localized inflationary pressures in housing and transportation. Additionally, tighter profit margins, global economic uncertainties, and the influx of new real estate supply could have potentially prompted financial institutions to take a more cautious approach to lending, mitigating risks and maintaining liquidity. This trend could have significant implications for Dubai’s real estate market. Higher borrowing costs could deter first-time buyers and residents, pushing demand further toward off-plan properties with attractive developer incentives and payment plans. This is a trend that warrants close monitoring over the coming quarters to assess its broader impact on the market dynamics.

Dubai Residential Off-Plan – A Force to be Reckoned With

Examining Dubai’s residential real estate supply reveals a striking trend: the volume of units under construction and in the planning phase, is rapidly approaching the total number of existing residential units.

Currently, Dubai boasts 556,760 existing residential units. In addition, there are 296,204 residential units under construction and another 41,785 in the planning phase.

Despite this rapid growth in supply, new off-plan projects continue to be launched at a remarkable pace. This highlights the confidence of developers in the market’s ability to absorb this influx of inventory. However, this relentless expansion also raises important considerations about potential market saturation and the pressure it may place on pricing dynamics, especially in certain high-density areas.

New Residential Unit Launches

No Dubai real estate market report would be complete without addressing the significant amount of supply entering the market in the upcoming years. As mentioned earlier, 2024 has undeniably proven to be the year for new off-plan development launches.

To date, a total of 129,265 new residential units have been launched or announced in 2024. In Q2 of this year, this figure stood at 78,361, meaning an additional 50,804 new residential units were introduced into the market in Q3 alone.

Current Supply Under Construction in Dubai

Let’s take a closer look at the dynamics of the off-plan market currently under construction. Of the 296,204 residential units under construction, 238,492 are apartments, 62,609 are villa/townhouses, and 5,163 are serviced apartments. This breakdown underscores the continued emphasis on apartment developments, reflecting both the demand for high-density housing and the evolving preferences of investors and end-users.

When broken down by unit size, the current construction pipeline reveals a significant emphasis on smaller units. Of the total units under construction, 49,193 are studios, 98,838 are one-bedroom units, 59,984 are two-bedroom units, 27,474 are three-bedroom units, 23,778 are four-bedroom units, 7,458 are five-bedroom units, and 3,404 are six-bedroom units.

Notably, studios and one-bedroom apartments account for nearly 50% of all units under construction, reflecting the continued demand for compact and affordable housing options. This trend aligns with the preferences of investors seeking high-yield properties, particularly in Dubai’s urban centers.

The Turning Point: Navigating Dubai's Market Shift Amidst New Supply

As previously noted, Q3 marked the beginning of a pivotal turning point in Dubai's real estate market, where signs of shifting dynamics began to emerge, setting the stage for the quarters and years ahead. This shift will continue to be driven by the ongoing completion of new supply being added to Dubai's existing residential stock over the next 18 to 24 months.

Year to date, a total of 22,672 units have been completed, with an additional 20,577 units scheduled for completion by the end of the year. However, it is likely that a large portion of these units will be delayed and pushed into 2025 due to construction setbacks and other factors.

A Record-Breaking Wave of New Supply

The Dubai residential market is on the brink of an unprecedented surge in new supply over the next three years. In 2025, an estimated 74,494 units are scheduled for completion, followed by 114,402 units in 2026, the largest annual number of estimated completed units Dubai has ever witnessed. In 2027, an additional 70,465 units are expected to enter the market.

These next few years represent the highest annual volume of completions in Dubai’s history, setting a new benchmark for the city’s real estate sector.

The scale of this supply influx is anticipated to have significant implications for market dynamics, potentially driving shifts in pricing, absorption rates, and overall sentiment, particularly in high-density areas. Over the next 18-24 months, the influx of new units is most likely to heighten competition and place downward pressure on prices in both the sales and rental markets.

Macroeconomic Factors and Population Growth

As of November 2024, the Central Bank of the UAE (CBUAE) has revised its inflation forecast for 2024, lowering it from 2.5% to 2.3%, with the same rate projected for 2025. This adjustment reflects lower-than-expected increases in commodity costs, incomes, and rents.

In Dubai, headline inflation moderated to 3.4% in the first quarter of 2024, below the global average, but accelerated to 3.9% in April, largely due to significant increases in transport prices and housing prices.

By October 2024, the UAE's inflation rate decreased to 2.38%, down from 2.50% in September, indicating a trend toward price stabilization.

These developments suggest that while inflationary pressures persist, particularly in sectors like transportation and housing, overall inflation in the UAE is trending downward, aligning with the CBUAE's revised forecasts.

As of November 2024, Dubai's population has continued its steady growth, reaching approximately 3.77 million residents. This increase aligns with the trend of adding around 100,000 new residents annually since the COVID-19 pandemic which reflects Dubai's ongoing appeal as a global hub for tourism, business, and residence.

Global Macroeconomic Factors and Their Impact on Dubai

On the global stage, macroeconomic factors continue to shape Dubai's economic landscape. The strength of the US dollar, to which the UAE dirham is pegged, has implications for trade, tourism, and investment flows. A strong dollar may make Dubai more expensive for tourists and investors from non-dollar-pegged countries, potentially impacting demand. Conversely, it enhances the city's attractiveness to dollar-based investors seeking stability in real estate and financial assets.

Additionally, the outcome of the 2024 US presidential election, particularly the re-election of Donald Trump, could introduce new geopolitical and economic dynamics. Policies favoring reduced trade restrictions and economic nationalism could influence global capital flows and investor sentiment. For Dubai, this could mean increased interest from US based investors and heightened regional demand, given the city's reputation as a safe haven during periods of global uncertainty.

On the downside, ongoing challenges such as the potential slowdown in the Chinese economy or rising interest rates in key global markets could weigh on foreign investment inflows. Nonetheless, Dubai's diversified economy and strategic location position it to capitalize on global shifts, leveraging its reputation as a leading hub for innovation, connectivity, and resilience.

Conclusion: A Transformative Quarter for Dubai Real Estate

Q3 2024 marked a defining moment in Dubai’s real estate journey, highlighting the market's resilience amid significant transformation. The significant growth of the off-plan segment, supported by record-breaking launches and innovative developer incentives, has shifted the spotlight, while the secondary market grapples with a recalibration driven by a transition to a buyer’s market. The surge in new supply, set to reach historic highs over the next three years, presents both opportunities and challenges, with pricing adjustments and market absorption likely to define the road ahead.

Despite global macroeconomic uncertainties and localized pressures, Dubai's real estate market remains a testament to resilience and a hub of opportunity. However, with record levels of new supply scheduled over the coming years and an ever-increasing number of launches, the risk of market saturation threatens large. The ability of the market to absorb this influx of inventory will be critical in determining its stability. While a growing population and Dubai’s global appeal provide strong foundations, the coming quarters and years will require careful attention to pricing strategies, absorption rates, and market dynamics. Stakeholders must tread cautiously in this transformative era, carefully managing growth to mitigate risks to ensure long-term stability of Dubai’s real estate market.